Release Date: April 3, 2026

Source: Industry Analysis / Fluorine Chemical Insight

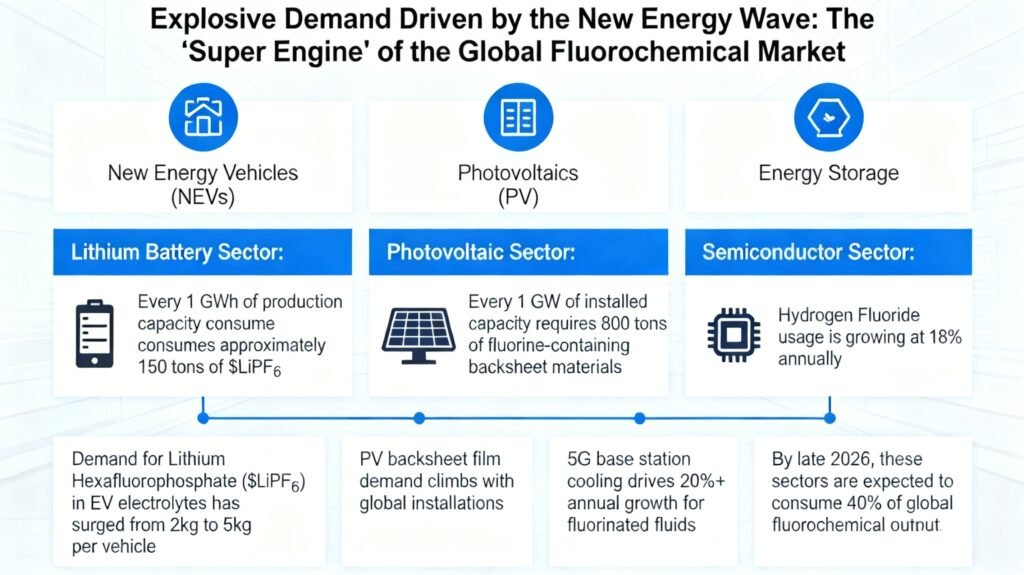

I. Explosive Demand Driven by the New Energy Wave

The “Super Engine” of the global fluorochemical market is now firmly powered by three core sectors: New Energy Vehicles (NEVs), Photovoltaics (PV), and Energy Storage. The demand for Lithium Hexafluorophosphate ($LiPF_6$) in EV electrolytes has surged from 2kg to 5kg per vehicle. Simultaneously, the demand for PV backsheet films is climbing in tandem with global installations, while the 5G base station cooling market is driving a 20%+ annual growth rate for fluorinated fluids. By late 2026, these sectors are expected to consume 40% of global fluorochemical output, marking a three-year peak in demand.

Lithium Battery Sector: Every 1 GWh of production capacity consumes approximately 150 tons of $LiPF_6$.

Photovoltaic Sector: Every 1 GW of installed capacity requires 800 tons of fluorine-containing backsheet materials.

Semiconductor Sector: Hydrogen Fluoride usage is growing at 18% annually, with demand increasing as chip manufacturing processes become more advanced.

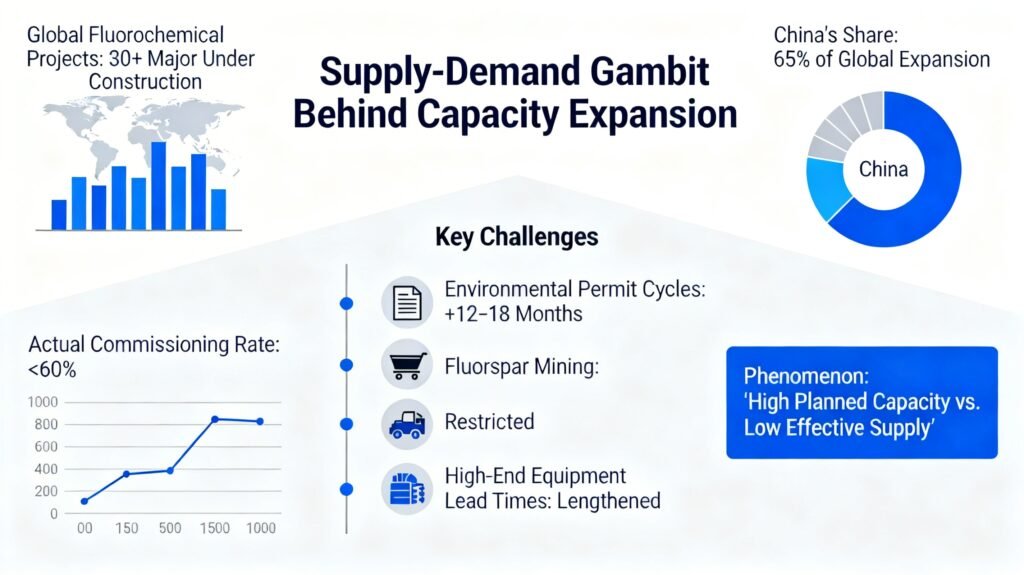

II. The Supply-Demand Gambit Behind Capacity Expansion

There are currently over 30 major fluorochemical projects under construction globally, with China accounting for 65% of this expansion. However, scaling up is facing significant friction: environmental permit cycles have extended by 12–18 months, fluorspar mining remains restricted, and lead times for high-end specialized equipment have lengthened. These factors have resulted in an actual commissioning rate of less than 60%, creating a unique phenomenon of “High Planned Capacity vs. Low Effective Supply.”

Environmental Costs: Environmental expenditures per ton of fluorochemical product have risen from 8% to 15% of total costs.

Technical Barriers: Electronic-grade Hydrofluoric Acid ($HF$) now requires a purity of 9N (99.9999999%), a standard that only five companies worldwide can consistently meet.

Regional Disparity: Demand growth in the Asia-Pacific is 2.3x faster than in Europe and the Americas, yet the capacity matching rate sits at only 68%.

III. Three Potential Scenarios for 2026

The Optimistic Scenario: If NEV penetration reaches 45% and annual PV installations exceed 300 GW, a supply gap of 150,000 tons will emerge. The primary shortages will be in high-end fluoropolymers (such as PFA, FEP, and ETFE) and electronic-grade fluorides.

The Neutral Scenario: If the phase-out of traditional refrigerants slows down and demand growth settles at 8%, the industry will maintain a tight balance. Common products like Aluminum Fluoride ($AlF_3$) may see phased surpluses.

The Pessimistic Scenario: If geopolitical tensions disrupt fluorspar exports or environmental regulations tighten further, industry-wide price volatility is likely. However, the probability of a systemic collapse in supply remains below 25%.

Conclusion: The industry is currently transitioning from “Scale Expansion” to “Value Upgrading.” Companies with deep technical reserves and ESG (Environmental, Social, and Governance) advantages are positioned to lead this new cycle.

Related Products